In today’s complex financial landscape, creating a comprehensive strategy for managing family finances is crucial. From budgeting to investments, this article explores practical tips to help families navigate their financial journey successfully.

Setting Financial Goals as a Family

When it comes to managing family finances, setting clear financial goals together is a crucial step towards a secure financial future. By establishing shared objectives, families can work towards building wealth, securing their financial well-being, and achieving their dreams.

Start by discussing and identifying short-term and long-term financial goals as a family. This could include saving for a family vacation, buying a new home, funding your children’s education, or planning for retirement. Make sure these goals are specific, measurable, achievable, relevant, and time-bound (SMART).

Encourage open communication and collaboration within the family to prioritize these goals. Each family member should have a role to play in contributing towards the financial goals. Consider holding regular family meetings to track progress, make adjustments if needed, and celebrate milestones achieved.

Moreover, it’s essential to establish a budget that aligns with your family’s goals. Track your income, expenses, and savings to ensure you are on the right path. Remember, financial goals may evolve over time, so regular review and adaptation are key to staying on track.

By setting financial goals as a family, you not only strengthen your financial foundation but also foster teamwork, discipline, and unity among family members. Together, you can navigate the complexities of family finances with confidence and purpose.

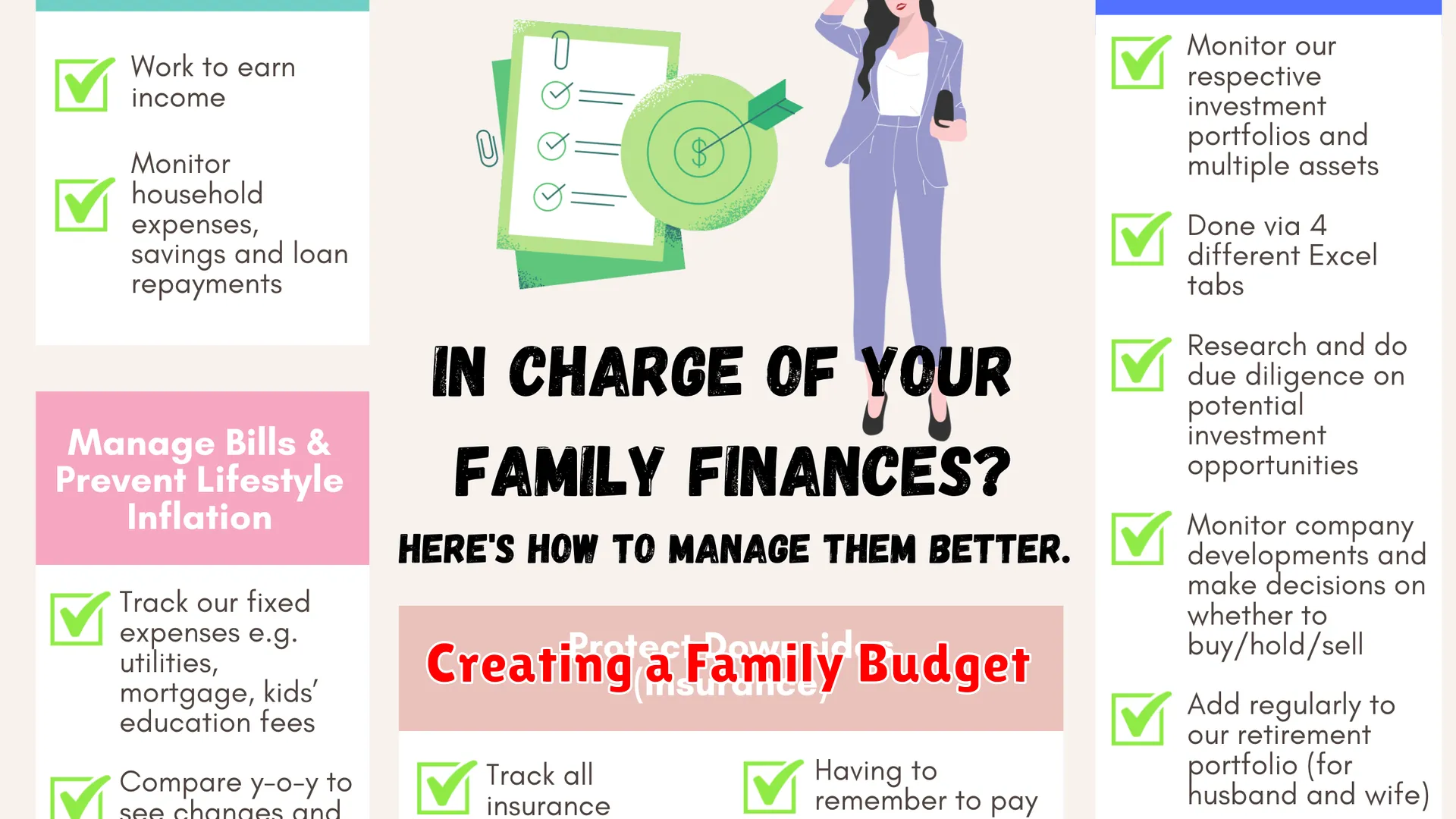

Creating a Family Budget

Establishing a family budget is a fundamental step in managing your household finances effectively. By creating a budget, you can gain a clearer understanding of your income and expenses, enabling you to make informed financial decisions and work towards achieving your financial goals.

Assess Your Income and Expenses

Start by determining all sources of income for your family, including salaries, bonuses, investments, and any other funds. Next, list down all your expenses such as mortgage or rent, utilities, groceries, transportation, insurance, and other regular bills.

Set Financial Goals

Define your financial goals as a family, whether it’s saving for a new home, education expenses, retirement, or a dream vacation. Having clear objectives in place will guide your budgeting decisions and help you prioritize your spending.

Create Categories and Allocate Funds

Organize your expenses into categories such as housing, groceries, transportation, saving, and entertainment. Allocate a specific amount of funds to each category based on your priorities and necessities. Remember to set aside money for emergency savings as well.

Monitor and Adjust Regularly

Regularly track your spending and compare it to your budget. Adjust your allocations as needed to ensure you are staying within your financial limits. Be proactive in identifying areas where you can cut back expenses or increase savings.

Seek Professional Advice

If you are struggling to create or stick to your budget, consider seeking financial advice from a professional. They can provide personalized guidance and strategies to improve your financial situation and help you achieve your long-term goals.

Managing Debt and Expenses

When it comes to navigating family finances effectively, managing debt and expenses plays a crucial role in ensuring financial stability and security for your household. Here are some key strategies to help you in this area:

- Create a Budget: Start by creating a detailed budget that outlines your income, expenses, and debt obligations. This will give you a clear picture of where your money is going and help you identify areas where you can cut back.

- Limit Credit Card Usage: Credit card debt can quickly spiral out of control. Try to limit your credit card usage and pay off your balances in full each month to avoid high interest charges.

- Set Financial Goals: Establish short-term and long-term financial goals for your family. Whether it’s building an emergency fund, saving for a major purchase, or paying off debt, having clear goals can help you stay motivated and track your progress.

- Consolidate Debt: If you have multiple debts with high interest rates, consider consolidating them into a single loan with a lower interest rate. This can help you save money on interest payments and simplify your debt repayment process.

- Negotiate with Creditors: If you’re struggling to meet your debt obligations, don’t hesitate to reach out to your creditors to discuss alternative payment arrangements or negotiate lower interest rates. Many creditors are willing to work with you to find a solution that works for both parties.

Investing for Your Family’s Future

When it comes to navigating family finances, one crucial aspect to consider is investing for your family’s future. This involves making strategic financial decisions that can provide long-term benefits and security for your loved ones.

One key strategy in investing for your family’s future is to start early. The power of compounding interest means that the earlier you begin investing, the more time your money has to grow. Encourage your family members, including children, to understand the importance of saving and investing from a young age.

Diversification is another essential principle when it comes to investing for your family’s future. By spreading your investments across different asset classes, industries, and geographic regions, you can reduce risk and increase the potential for returns over time.

Setting clear financial goals is also crucial in this strategy. Whether your objective is to save for your children’s education, a down payment on a house, or a comfortable retirement, having specific goals can help you stay focused and disciplined in your investment approach.

Regularly reviewing and adjusting your investment portfolio is a necessary step in navigating family finances. Life circumstances, market conditions, and financial goals can change over time, so it’s essential to reassess your investments periodically to ensure they align with your family’s evolving needs.

By incorporating these principles and strategies into your financial planning, you can work towards building a secure and prosperous future for your family through smart and strategic investing.

Teaching Financial Literacy to Children

Teaching financial literacy to children is a crucial aspect of preparing them for a successful future. It involves instilling an understanding of basic financial concepts and practices from a young age. Here are some effective strategies to help children build a strong foundation in financial literacy:

Start Early and Make It Fun

Introducing financial concepts to children at an early age can set the stage for their financial well-being in the future. Use age-appropriate games, activities, and real-life examples to make learning about money engaging and enjoyable. Encourage them to save a portion of their allowance or earnings in a piggy bank or savings account.

Lead by Example

Children learn by observing their parents’ behaviors and attitudes towards money. Be a positive role model by demonstrating responsible financial habits, such as budgeting, saving, and avoiding impulsive purchases. Involve children in age-appropriate discussions about family finances to help them understand the value of money.

Teach Budgeting and Smart Spending

Help children understand the importance of budgeting by setting a clear allowance structure and introducing the concept of needs versus wants. Encourage them to prioritize their spending decisions and discuss the consequences of impulsive buying. Teach them to compare prices, look for deals, and save up for larger purchases.

Introduce the Basics of Investing

As children grow older, introduce them to the basics of investing and the power of compound interest. Help them open a mock investment account or explore virtual investing platforms to learn about stocks, bonds, and the concept of risk and return. Encourage them to set financial goals and track their progress over time.

Emphasize the Importance of Giving Back

Teach children the value of generosity and the impact of charitable giving. Encourage them to donate a portion of their allowance to a cause they care about or participate in community service activities. By fostering a spirit of giving, children can develop empathy, gratitude, and a sense of social responsibility.

Conclusion

In conclusion, implementing a comprehensive family financial strategy is crucial for long-term stability and security.

{kind=link}