Embark on your financial journey with “The Beginner’s Roadmap to Financial Planning,” a comprehensive guide for mastering money management and securing your financial future.

Assessing Your Financial Health

Assessing your financial health is a crucial step in creating a solid financial plan. It involves taking a close look at your current financial situation to understand where you stand and what steps you need to take to improve.

1. Calculate Your Net Worth

Calculate your net worth by determining the total value of your assets (such as savings, investments, properties) and subtracting your liabilities (debts, loans). A positive net worth indicates financial stability, while a negative one may signal potential financial trouble.

2. Review Your Income and Expenses

Review your income sources and monthly expenses. Make sure your income covers your essential expenses and allows for savings and investments. Identifying any discrepancies can help you adjust your budget and spending habits.

3. Check Your Savings and Emergency Fund

Assess the adequacy of your savings and emergency fund. A strong emergency fund should cover at least three to six months’ worth of living expenses. If your savings fall short, prioritize building this fund to handle unexpected financial challenges.

4. Evaluate Your Debt Level

Evaluate your debt level by considering the types of debts you have, their interest rates, and repayment terms. High-interest debts or excessive debts relative to your income can hinder your financial health. Develop a plan to repay debts efficiently.

5. Check Your Retirement Savings

Check your retirement savings progress and assess if you are on track to meet your retirement goals. Consider factors such as your age, desired retirement lifestyle, and retirement account contributions to ensure a comfortable retirement.

By assessing these key aspects of your financial health, you can identify areas for improvement and make informed decisions to secure your financial future.

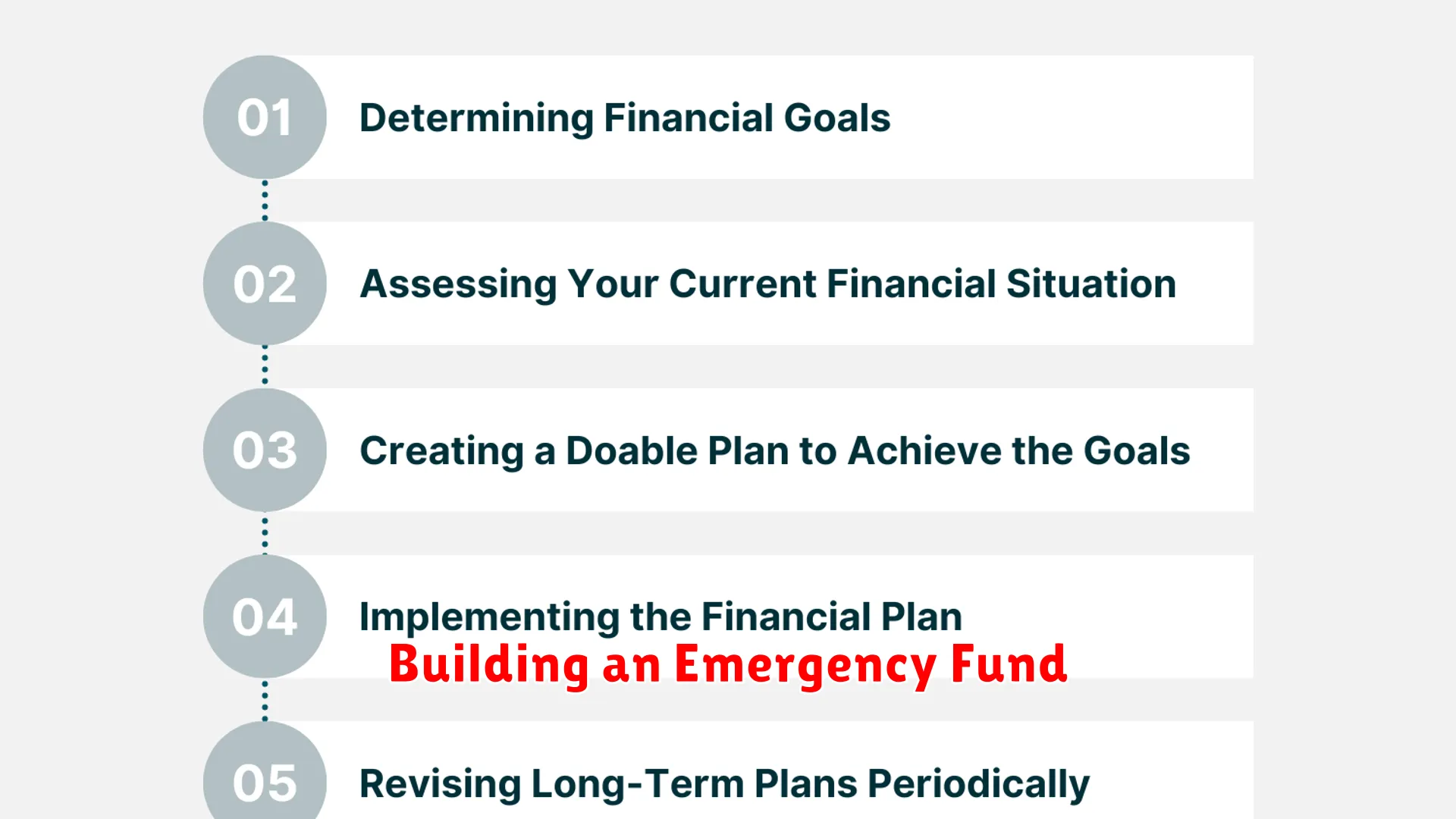

Setting Realistic Financial Goals

Setting realistic financial goals is an essential step in a successful financial planning journey. When setting financial goals, it’s important to ensure they are specific, measurable, achievable, relevant, and time-bound – known as the SMART criteria.

Begin by evaluating your current financial situation and identifying areas where you want to improve. Whether it’s saving for a vacation, paying off debt, or investing for retirement, your goals should align with your priorities and values.

Consider breaking down larger goals into smaller, manageable milestones. This approach can help you stay motivated and track your progress effectively. Celebrate each achievement, no matter how small, to stay engaged in your financial plan.

Moreover, be realistic when setting timelines for your goals. Understand that some goals may take longer to achieve than others, and setbacks may occur along the way. Flexibility and adaptability are key to staying on course.

Regularly review and adjust your financial goals as your circumstances change. Life events, economic conditions, and personal priorities may influence your goals over time. By staying proactive and flexible, you can ensure that your financial goals remain relevant and attainable.

Building an Emergency Fund

Building an emergency fund is a crucial step in your financial planning journey. An emergency fund acts as a safety net to protect you from unexpected financial burdens and emergencies, such as medical expenses, car repairs, or sudden job loss.

To start building your emergency fund, establish a realistic savings goal. It’s recommended to have at least three to six months’ worth of living expenses saved. Calculate your monthly expenses and set aside a portion of your income to contribute to this fund regularly.

Consider opening a separate savings account specifically for your emergency fund. This separation can help prevent you from dipping into the fund for non-emergencies and keep the money easily accessible when needed.

Automate your savings by setting up automatic transfers from your checking account to your emergency fund. This way, you ensure consistent contributions without having to remember to save each month.

Remember that building an emergency fund requires discipline and patience. Start small if needed, but stay committed to reaching your savings goal. Having this financial cushion will provide you with peace of mind and financial security in times of uncertainty.

Diversifying Your Investment Portfolio

When it comes to financial planning, one key strategy for beginners is diversifying your investment portfolio. This involves spreading your investments across different asset classes to reduce risk and potentially increase returns.

The Importance of Diversification

Diversification helps minimize the impact of a decline in any single investment on your overall portfolio. By investing in a mix of assets such as stocks, bonds, real estate, and commodities, you can help safeguard your investments against market volatility.

How to Diversify

Begin by assessing your risk tolerance and financial goals. This will guide you in determining the right mix of investments for your portfolio. Consider allocating your assets across different industries, geographic locations, and investment types to create a well-rounded portfolio.

Benefits of Diversification

Not only does diversification reduce risk, but it also opens up opportunities for growth. When one asset class underperforms, another may outperform, balancing your overall returns. Diversification can help you achieve a more stable and long-term financial outlook.

Regularly Reviewing and Adjusting Your Plan

Financial planning is not a one-time thing, it requires consistent review and adjustments to stay on track towards your goals. As a beginner, it’s important to regularly revisit your financial plan to make sure it aligns with your current financial situation and future aspirations.

By reviewing your plan regularly, you can assess if you are meeting your savings targets, identify any areas where you may be overspending, and make necessary adjustments to your budget or investments. This process allows you to stay proactive in managing your finances and make informed decisions to achieve your long-term financial objectives.

Consider setting a specific schedule, such as monthly or quarterly, to review your financial plan. During these reviews, take note of any changes in your income, expenses, or financial goals, and adjust your plan accordingly. It’s also crucial to reassess your risk tolerance and investment strategies to ensure they are still suitable for your current situation.

Conclusion

Creating a solid financial plan is crucial for a secure future. By following these beginner steps, you can start your journey towards financial stability and success.

{kind=link}