Discover how to make the most of credit card rewards while avoiding debt traps. Learn strategies for maximizing benefits and smart spending habits in “Credit Card Smarts: Maximizing Rewards and Minimizing Debt.”

Choosing the Right Credit Card

When it comes to credit cards, it’s essential to choose the right one that aligns with your financial goals. Here are some key points to consider to help you make an informed decision:

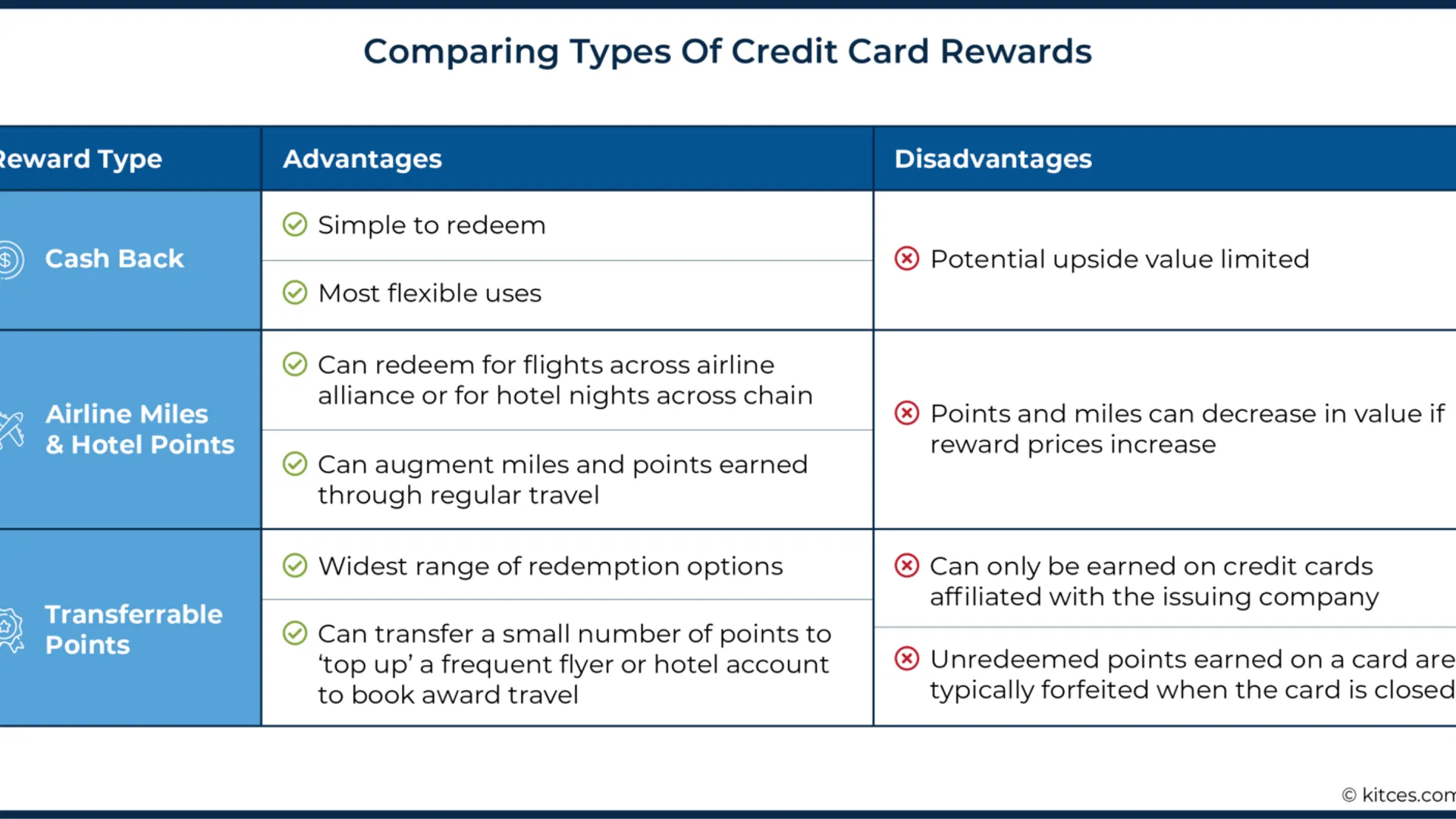

- Rewards Program: Look for a credit card that offers rewards that match your spending habits. Whether you prefer cashback, travel miles, or points for specific retailers, choose a card that maximizes benefits based on your lifestyle.

- Interest Rates: Pay attention to the Annual Percentage Rate (APR) offered by the credit card. Lower interest rates can save you money in the long run, especially if you tend to carry a balance on your card.

- Fees and Charges: Be aware of the various fees associated with the credit card, such as annual fees, late payment fees, or foreign transaction fees. Opt for a card with minimal fees to avoid unnecessary expenses.

- Credit Limit: Consider your spending habits and financial discipline when choosing a credit limit. It’s important to have a limit that allows you to make necessary purchases without exceeding your budget.

- Credit Score Impact: Some credit cards are designed for individuals with excellent credit scores, while others cater to those looking to build or rebuild their credit. Choose a card that suits your credit history to improve your overall financial health.

By carefully evaluating these factors, you can select a credit card that not only maximizes rewards but also helps you minimize debt and manage your finances effectively.

Understanding Reward Programs

When it comes to maximizing rewards and minimizing debt with credit cards, understanding reward programs is essential. Reward programs offered by credit card companies can provide you with various benefits such as cashback, travel points, or discounts on purchases.

First and foremost, it’s important to comprehend how the reward system works for your specific credit card. Different cards have different reward structures, earning rates, and redemption options. Some cards may offer bonus points for specific categories like dining, groceries, or gas, while others provide a flat-rate on all purchases.

Monitoring your spending is crucial to make the most out of reward programs while avoiding accumulating debts. By keeping track of your expenses and paying off your balance in full each month, you can benefit from rewards without falling into debt traps and incurring high interest charges.

Furthermore, strategically using your credit card for everyday expenses and bills can help you earn more rewards. Consider consolidating your spending on a single credit card with the most advantageous rewards for your spending habits to maximize the benefits.

Regularly reviewing your reward balances and staying updated on any promotions or offers from the credit card issuer can also help you take advantage of additional perks and bonuses. Being aware of any changes in the reward program can ensure you are making the most informed decisions.

Tips for Managing Credit Card Debt

When it comes to credit card usage, it’s essential to have a strategy in place to effectively manage your debt while also maximizing rewards. Here are some valuable tips to help you navigate this balancing act:

- Create a Budget: Start by assessing your income and expenses to set a clear budget. Knowing how much you can afford to spend each month will prevent overspending and accumulating unnecessary debt.

- Pay On Time, In Full: One of the most crucial tips for managing credit card debt is to pay your bills on time and ideally in full. By doing so, you avoid costly interest charges and maintain a good credit score.

- Avoid Minimum Payments: While minimum payments are tempting, they can lead to a cycle of debt. Always aim to pay more than the minimum amount due to reduce your overall balance faster.

- Monitor Your Spending: Keep track of your credit card transactions regularly to ensure you stay within your budget. This practice will also help you identify any unnecessary expenses that can be cut down.

- Utilize Rewards Wisely: Take advantage of credit card rewards programs to earn cash back, points, or miles. However, be cautious not to overspend just to earn rewards, as this can counteract your debt management efforts.

- Consider Balance Transfers: If you have high-interest debt on one card, transferring it to a card with a lower interest rate can save you money. But be mindful of transfer fees and terms to make an informed decision.

- Seek Professional Help if Needed: If managing your credit card debt becomes overwhelming, don’t hesitate to seek advice from a financial advisor or credit counselor. They can provide guidance on debt repayment strategies tailored to your situation.

By incorporating these tips into your financial routine, you can effectively manage your credit card debt while optimizing the benefits of using credit cards responsibly.

Avoiding Common Credit Card Pitfalls

When it comes to managing credit cards effectively, avoiding common pitfalls is key to maximizing rewards and minimizing debt. By being aware of these pitfalls and taking proactive measures, you can make the most of your credit card benefits while staying financially healthy.

1. Paying Only the Minimum Balance

One common credit card pitfall is paying only the minimum balance each month. While it may seem convenient in the short term, it can lead to substantial interest payments over time. Always strive to pay more than the minimum required to reduce your overall debt.

2. Ignoring Due Dates

Missing credit card payment due dates can result in late fees and negative impacts on your credit score. Set up payment reminders or automatic payments to ensure you never miss a due date. Timely payments are crucial for maintaining a healthy credit history.

3. Overspending to Earn Rewards

While credit card rewards can be enticing, be careful not to overspend just to earn points or cash back. Make sure your purchases align with your budget and financial goals. The value of rewards should never outweigh the cost of accumulating debt.

4. Carrying a High Balance

Carrying a high balance on your credit card can result in high interest charges and impact your credit utilization ratio. Aim to keep your credit utilization below 30% of your total available credit to maintain a positive credit score.

5. Falling for Hidden Fees

Many credit cards come with hidden fees, such as annual fees, balance transfer fees, or foreign transaction fees. Read the fine print and understand all potential fees associated with your card to avoid surprises. Look for cards with transparent fee structures.

Strategies for Paying Off Balances

When it comes to managing credit card debt, having a clear repayment plan is crucial. Here are some effective strategies for paying off balances and regaining financial control:

1. Create a Budget

Start by evaluating your monthly income and expenses to determine how much you can allocate towards paying off your credit card balances. Creating a realistic budget will help you stay on track and avoid accumulating more debt.

2. Prioritize High-Interest Cards

Focus on paying off credit cards with the highest interest rates first. By tackling these balances, you can reduce the overall amount you’ll pay in interest over time, saving you money in the long run.

3. Make More than Minimum Payments

Avoid the minimum payment trap by striving to pay more than the minimum amount due each month. By making larger payments, you can accelerate the payoff process and reduce the total interest accrued.

4. Consider a Balance Transfer

If you’re struggling with high-interest debt, a balance transfer to a card with a lower interest rate can be a strategic move. Just ensure you understand the terms and any transfer fees involved.

5. Seek Debt Repayment Assistance

Don’t hesitate to seek help from credit counseling services or debt repayment programs if you feel overwhelmed by your balances. These resources can provide guidance and support in creating a repayment plan.

Conclusion

In conclusion, managing credit card usage wisely by maximizing rewards and minimizing debt is essential for financial wellness and smart money management.

{kind=link}