Transitioning from renting to owning a home is a significant financial journey that requires careful planning and consideration. In this article, we will explore the steps and strategies to help you successfully navigate the path to homeownership.

Assessing Rent vs. Buy Decision

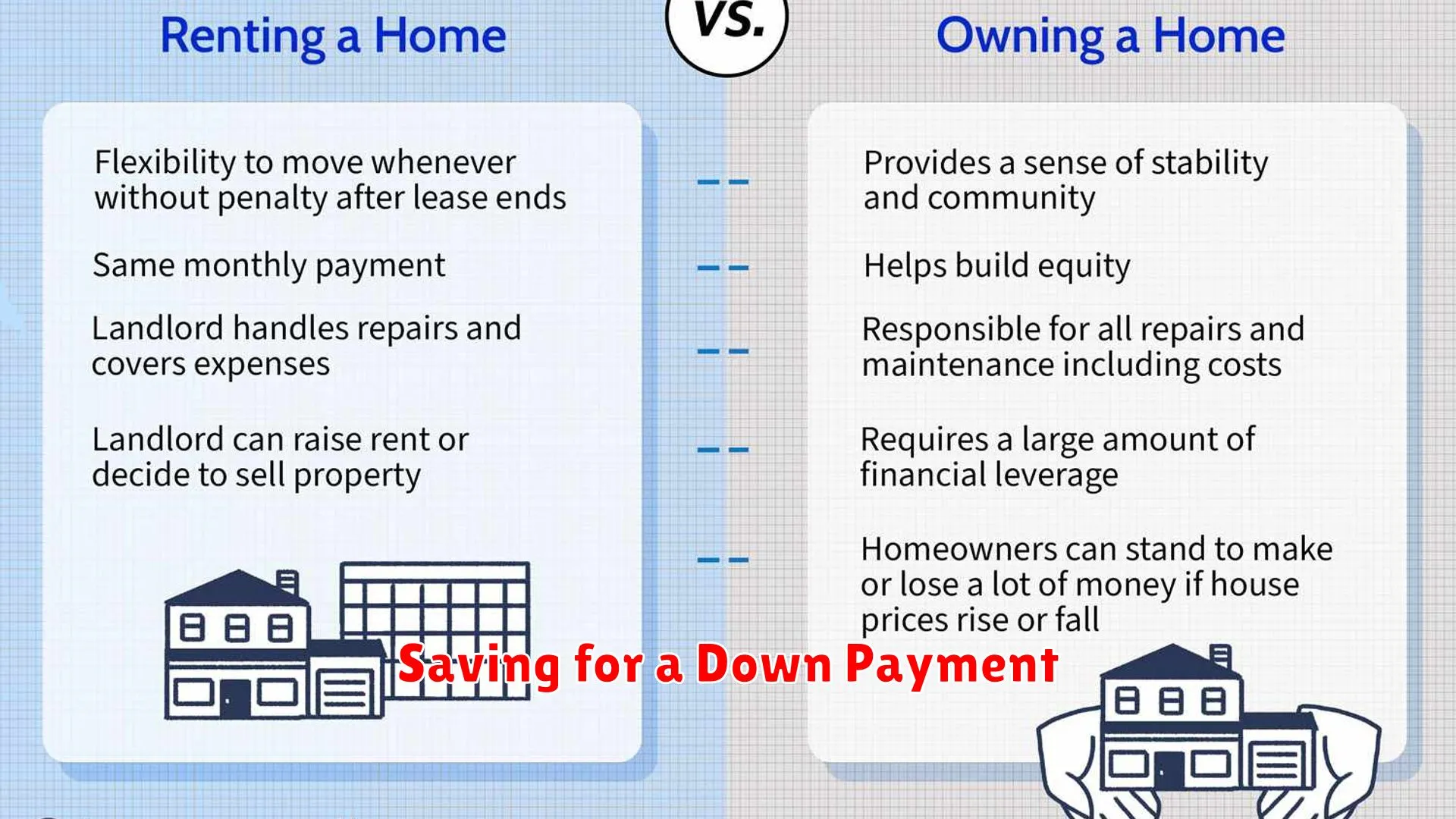

When considering the transition from renting to owning a home, one crucial aspect to evaluate is the rent vs. buy decision. This assessment involves comparing the advantages and disadvantages of renting a property versus purchasing one, taking into account various financial factors.

One key factor to analyze is financial stability and long-term goals. Renting may offer flexibility in the short term, but owning a home can provide long-term financial security and equity build-up. Assess your current financial situation and future objectives to determine which option aligns best with your needs.

Another aspect to consider is market conditions and property value trends. Research the real estate market in your desired location to understand whether it favors renters or buyers. Assessing the potential for property appreciation can influence your decision-making process.

Furthermore, the cost comparison between renting and buying plays a significant role. While renting may involve fixed monthly payments, homeownership includes additional expenses such as mortgage payments, property taxes, insurance, and maintenance costs. Calculate the total cost of each option to determine which is more financially feasible in the long run.

Saving for a Down Payment

One of the most crucial steps in transitioning from renting to owning a home is saving for a down payment. This financial milestone is a key requirement for most home purchases and can significantly impact your ability to secure a mortgage with favorable terms. Here are some essential strategies to help you save for a down payment:

Set a Clear Savings Goal

Start by determining how much you need to save for a down payment based on the price range of homes you are considering. Setting a specific savings target will give you a clear objective to work towards.

Create a Budget and Cut Expenses

Review your current spending habits and identify areas where you can cut back to allocate more funds towards your down payment fund. Consider reducing dining out, subscription services, or unnecessary purchases.

Automate Your Savings

Set up automatic transfers from your checking account to a separate savings account dedicated to your down payment. This automated process can help you consistently grow your savings without the temptation to spend the money elsewhere.

Explore Down Payment Assistance Programs

Research government programs, grants, or loans that offer assistance with down payments for first-time homebuyers. These programs can help bridge the gap between your savings and the required down payment amount.

Consider Alternative Sources of Income

Explore opportunities to increase your income through side gigs, freelance work, or selling items you no longer need. Additional sources of income can boost your savings rate and accelerate your progress towards your down payment goal.

Understanding Mortgage Options

When transitioning from renting to owning a home, one of the crucial aspects to consider is understanding mortgage options. Mortgages are loans specifically designed for purchasing real estate, allowing individuals to buy a property without having to pay the full purchase price upfront.

Fixed-Rate Mortgage

A fixed-rate mortgage offers stable monthly payments over the life of the loan. This means the interest rate remains constant, providing predictability for budgeting purposes. It is a popular choice for homeowners who prefer consistent payments.

Adjustable-Rate Mortgage

Alternatively, an adjustable-rate mortgage (ARM) typically starts with a lower initial interest rate that may adjust periodically based on market conditions. While initial payments may be lower, there is the potential for increased payments in the future.

Government-Backed Loans

Government-backed loans, such as those offered by the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), provide options for individuals with less-than-perfect credit or a limited down payment. These loans often come with lower down payment requirements compared to conventional mortgages.

Jumbo Loans

Jumbo loans are used when purchasing high-priced properties that exceed the loan limits set by government-sponsored entities. These loans typically require a higher down payment and have stricter approval requirements due to the larger loan amount.

Consider Your Financial Goals

When choosing a mortgage option, it is essential to align your financial goals with the terms of the loan. Factors such as your credit score, down payment amount, and long-term homeownership plans should all be taken into consideration to determine the most suitable mortgage for your situation.

Budgeting for Homeownership Costs

Transitioning from renting to owning a home can be an exciting journey, but it also comes with financial responsibilities that need careful planning. One crucial aspect to consider is budgeting for homeownership costs to ensure a smooth transition and sustainable homeownership.

Here are some key factors to consider when budgeting for homeownership costs:

- Mortgage Payments: The largest component of homeownership costs is usually the monthly mortgage payment. It’s important to factor in not just the principal and interest but also property taxes, homeowner’s insurance, and private mortgage insurance (if applicable).

- Utilities and Maintenance: Budgeting for ongoing expenses like utilities (electricity, water, gas) and maintenance costs is essential. Homeownership may come with additional expenses such as lawn care, pest control, and repairs.

- Homeowners Association (HOA) Fees: If your home is part of a community with an HOA, be sure to include the monthly or annual fees in your budget. These fees typically go towards maintaining shared spaces and amenities.

- Emergency Fund: It’s advisable to have an emergency fund set aside specifically for homeownership-related emergencies, such as a leaky roof or a broken appliance. Having savings for unexpected expenses can provide peace of mind.

- Property Taxes: Property taxes can vary significantly based on location and the value of the property. Make sure to research the property tax rates in your area and include this expense in your budget.

By creating a detailed budget that includes all these homeownership costs, you can better prepare yourself financially for the transition from renting to owning a home. Remember, being proactive and planning ahead can help you enjoy the benefits of homeownership while staying financially stable.

Planning for Long-Term Home Maintenance

When transitioning from renting to owning a home, planning for long-term home maintenance is crucial to protect your investment and ensure the longevity of your property. Here are some key considerations:

Create a Maintenance Budget

Setting aside funds for home maintenance is essential. Plan for regular maintenance tasks like HVAC servicing, roof inspections, and landscaping to prevent costly repairs down the line.

Stay Proactive with Repairs

Addressing minor repairs promptly can prevent them from turning into major issues. Keep a list of home repair tasks and schedule regular inspections to catch problems early.

Invest in Quality Materials

When upgrading or renovating your home, opt for quality materials that are durable and long-lasting. This can reduce the need for frequent repairs and replacements.

Consider Home Warranty Plans

Home warranty plans can provide peace of mind by covering the cost of repairs or replacements for major systems and appliances. Research different warranty options to find the best fit for your home.

Conclusion

Transitioning from renting to owning a home requires careful financial planning and commitment. By saving for a down payment, maintaining a good credit score, and understanding the full cost of homeownership, individuals can set themselves on a successful path to becoming homeowners.

{kind=link}