Embark on a journey through the intricate landscape of student loans with our comprehensive guide, offering insights and strategies for navigating this essential aspect of higher education financing.

Understanding Different Types of Student Loans

When navigating the world of student loans, it’s essential to understand the various types of loans available to students. Here are some common types of student loans:

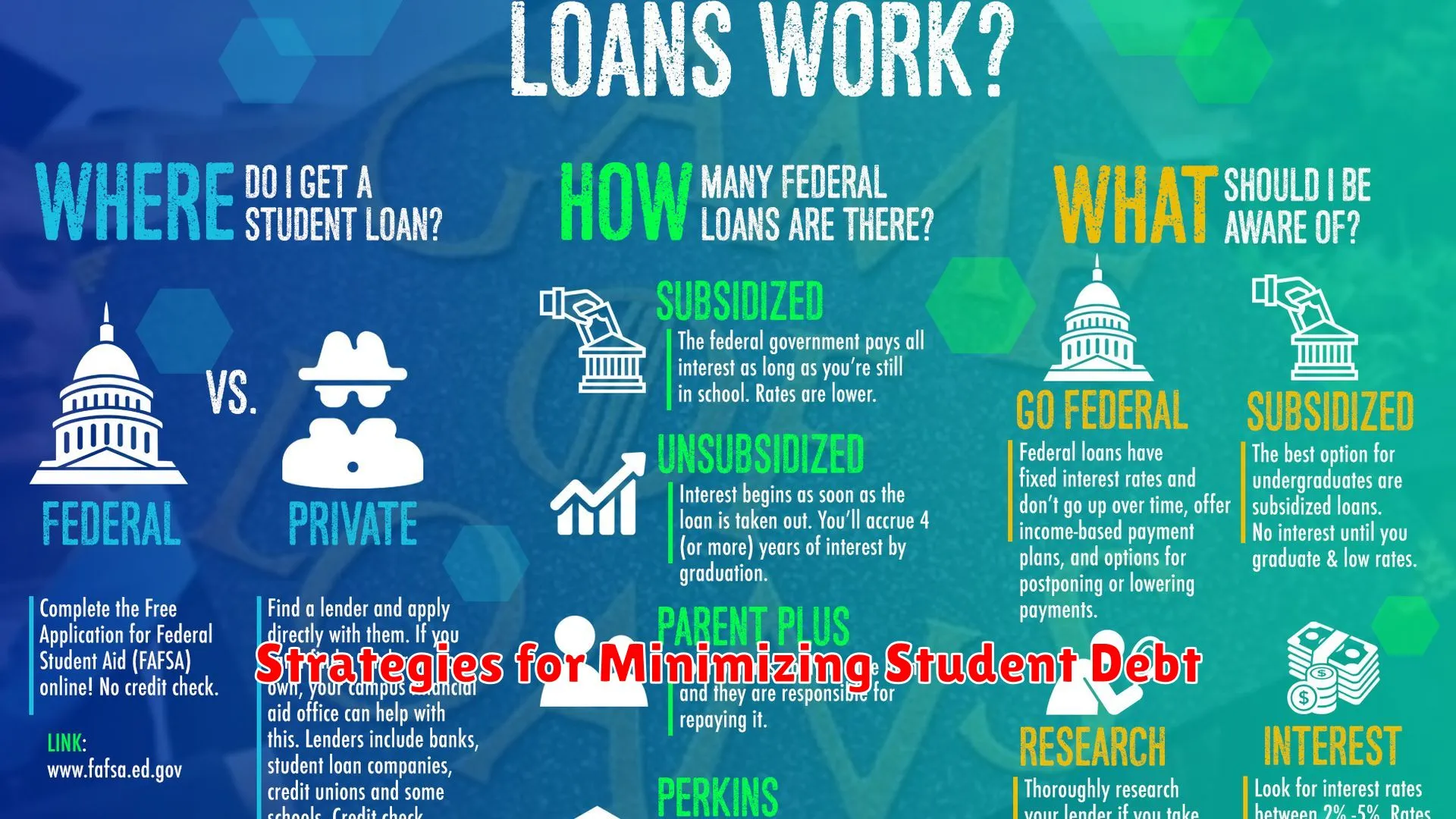

Federal Student Loans

Federal student loans are loans offered by the government and typically have lower interest rates compared to private loans. They include Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans.

Private Student Loans

Private student loans are offered by private lenders such as banks or credit unions. These loans may have higher interest rates and less flexible repayment options than federal loans.

Parent PLUS Loans

Parent PLUS Loans are federal loans available to parents of dependent undergraduate students. These loans can help parents cover the cost of their child’s education.

Perkins Loans

Perkins Loans are low-interest federal student loans for undergraduate and graduate students with exceptional financial need. However, the Perkins Loan program has been discontinued.

Consolidation Loans

Consolidation loans allow borrowers to combine multiple federal student loans into one new loan. This can simplify repayment by combining multiple payments into one.

Strategies for Minimizing Student Debt

As you navigate the world of student loans, it’s essential to have a plan in place to minimize your overall student debt burden. Here are some effective strategies to help you manage and reduce your student debt:

Create a Budget and Stick to It

One of the key ways to minimize student debt is by creating a budget and sticking to it religiously. By tracking your expenses and income, you can better manage your finances and avoid unnecessary spending.

Apply for Scholarships and Grants

Seek out scholarships and grants to help offset the cost of tuition. These forms of financial aid do not require repayment, making them an excellent way to reduce your overall student debt.

Work Part-Time During School

Consider working part-time while in school to help cover your expenses. This can help reduce the amount of loans you need to take out, ultimately lowering your debt burden after graduation.

Explore Federal Loan Options

Before turning to private loans, explore federal loan options, such as Direct Subsidized or Unsubsidized Loans. These loans often come with lower interest rates and more flexible repayment terms.

Consider Income-Driven Repayment Plans

If you find yourself struggling with high monthly loan payments after graduation, consider enrolling in an income-driven repayment plan. These plans base your monthly payment on your income, making it more manageable.

Avoid Unnecessary Borrowing

Lastly, to minimize student debt, only borrow what is absolutely necessary. Avoid taking out loans for non-essential expenses like vacations or luxury items, as these can quickly add up and contribute to a higher debt load.

Repayment Plan Options

When it comes to paying off your student loans, understanding the various repayment plan options available to you is crucial. Here’s a breakdown of some of the most common repayment plans to help you make an informed decision:

1. Standard Repayment Plan

The standard repayment plan is the most straightforward option, where you make fixed monthly payments over a set period of time. While this plan typically results in higher monthly payments, it can help you pay off your loans faster and with less interest in the long run.

2. Income-Driven Repayment Plans

Income-driven repayment plans adjust your monthly payments based on your income, making them more manageable if you’re facing financial challenges. There are several types of income-driven plans, such as Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR).

3. Graduated Repayment Plan

Under a graduated repayment plan, your payments start lower and increase over time, usually every two years. This can be beneficial if you expect your income to grow steadily in the future.

4. Extended Repayment Plan

The extended repayment plan allows you to extend your repayment period beyond the standard 10 years, resulting in lower monthly payments. Keep in mind that while this option reduces your monthly payment amount, you may end up paying more in interest over the life of the loan.

5. Consolidation Loans

Consolidating your loans involves combining multiple federal loans into one for a single monthly payment. This can simplify your repayment process and potentially lower your monthly payment through an extended repayment term.

Choosing the right repayment plan is essential for managing your student loan debt effectively. Consider your financial situation, long-term goals, and the eligibility requirements for each plan before making a decision.

Loan Forgiveness Programs

Loan forgiveness programs offer a valuable opportunity for borrowers to potentially eliminate a portion or all of their student loan debt under specific circumstances. These programs are designed to alleviate the financial burden faced by individuals who have taken out student loans but are struggling to repay them.

Federal Loan Forgiveness Programs

The federal government offers various loan forgiveness programs, including the Public Service Loan Forgiveness (PSLF) program, which forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments while working full-time for a qualifying employer in public service.

Income-Driven Repayment Plans

Income-Driven Repayment (IDR) plans provide another avenue for loan forgiveness. These plans adjust your monthly payments based on your income and family size. After making payments for a certain period, usually 20 or 25 years, any remaining balance may be forgiven, although taxes may be applicable on the forgiven amount.

Teacher Loan Forgiveness

Teachers may be eligible for the Teacher Loan Forgiveness program, which forgives up to a certain amount of their federal student loans if they teach full-time for five complete and consecutive years in a low-income school or educational service agency.

State-Specific Forgiveness Programs

Some states offer their own loan forgiveness programs for residents who meet specific criteria, such as working in certain high-demand fields or underserved areas. These programs can provide additional relief, so it’s worth researching what options are available in your state.

Managing Loans After Graduation

Once you graduate from college, managing your student loans becomes a critical aspect of your financial journey. Here are some essential tips to help you navigate the world of student loans effectively:

Create a Repayment Plan

Start by understanding the terms of your loans and create a repayment plan that fits your financial situation. Consider options such as income-driven repayment plans or refinancing to make payments more manageable.

Stay Organized

Keep track of all your loan documents, correspondence, and payment schedules. Setting up automatic payments can help you avoid missing deadlines and facing penalties.

Budget Wisely

Develop a budget that accounts for loan payments along with your other expenses. Prioritize your loans to ensure they are paid on time and in full each month.

Explore Forgiveness Programs

Look into forgiveness programs for specific professions, such as public service or teaching. These programs can help reduce or eliminate your remaining loan balance after meeting certain criteria.

Communicate with Your Lender

If you experience financial hardship or difficulty making payments, don’t hesitate to reach out to your lender. They may offer temporary relief options or modifications to help you stay on track.

Remember, managing your student loans responsibly is crucial for your long-term financial stability. By staying informed and proactive, you can successfully navigate the world of student loans and achieve your financial goals.

Conclusion

Understanding student loans is crucial for successful financial planning during college years.

{kind=link}