Embarking on the journey to financial independence can be both daunting and exhilarating for millennials. In this guide, we explore practical tips and strategies to help young adults achieve financial freedom and build a secure future.

Setting Financial Goals

In the journey towards financial independence, setting clear financial goals is crucial for millennials. By defining what you aim to achieve, you can create a roadmap that guides your decisions and actions.

Start by assessing your current financial situation. Understand your income, expenses, and debts. This self-awareness forms the foundation for setting realistic financial goals that align with your circumstances.

Next, prioritize your objectives. Whether it’s building an emergency fund, paying off student loans, saving for a home, or investing for retirement, establish financial goals that are specific, measurable, achievable, relevant, and time-bound (SMART).

Consider breaking down long-term goals into smaller milestones. Celebrating these achievements along the way can keep you motivated and on track towards financial independence.

Remember, financial goals are not set in stone. Regularly review and adjust them as your circumstances evolve. Flexibility is key to ensuring your goals remain realistic and attainable.

Mastering Budgeting and Saving

For millennials striving for financial independence, mastering budgeting and saving is essential. Creating a budget allows you to take control of your money and track where it is being spent. Start by listing all your sources of income and then break down your expenses into categories such as rent, utilities, groceries, entertainment, and savings. Be sure to prioritize saving in your budget to ensure you are setting aside money for the future.

One effective strategy for budgeting is the 50/30/20 rule. Allocate 50% of your income to essentials like rent and bills, 30% to discretionary expenses like dining out and entertainment, and 20% to savings or paying off debt. By following this guideline, you can maintain a balanced financial plan that promotes both spending and saving.

When it comes to saving, establishing an emergency fund should be a top priority. Aim to set aside at least three to six months’ worth of expenses in case of unexpected events like medical emergencies or job loss. Another effective way to save is by automating your savings – set up automatic transfers to your savings account each time you receive a paycheck.

Additionally, consider cutting back on unnecessary expenses to increase your saving potential. This may involve reducing dining out, canceling unused subscriptions, or finding more affordable alternatives for your everyday needs. By being mindful of your spending habits and making conscious choices, you can free up more money to put towards your savings goals.

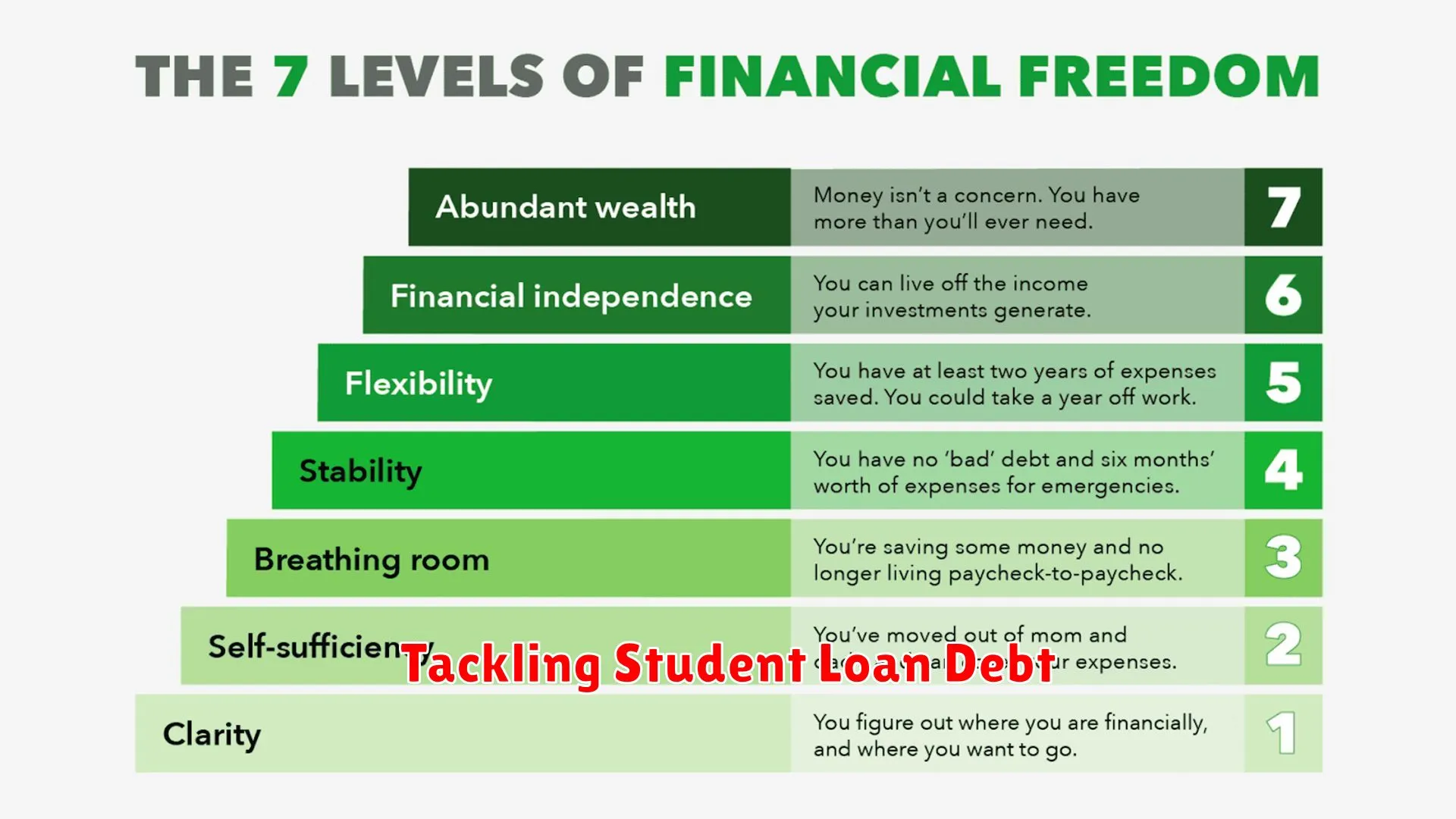

Tackling Student Loan Debt

Student loan debt can be a significant hurdle for millennials striving for financial independence. Here are some strategies to help tackle this burden:

Evaluate Your Loans

Start by understanding the details of your student loans, including the amount you owe, the interest rates, and the repayment terms. This information will give you a clear picture of your overall debt and help you plan effectively.

Create a Budget

Develop a realistic budget that outlines your income, expenses, and debt payments. Prioritize your student loan payments within your budget to ensure you are making progress in reducing your debt.

Explore Repayment Options

Look into income-driven repayment plans or loan consolidation options that can make your monthly payments more manageable. Some programs offer loan forgiveness after a certain period of time.

Increase Your Income

Consider finding ways to boost your income, such as starting a side hustle, freelancing, or taking on additional work. The extra money can be dedicated towards paying off your student loans faster.

Reduce Expenses

Cutting back on non-essential expenses can free up more money to put towards your student loans. Review your spending habits and identify areas where you can make adjustments to save more.

Seek Financial Assistance

Don’t hesitate to seek guidance from financial advisors or student loan counselors who can provide expert advice and help you navigate your repayment options effectively.

Investing in Your Future

As a millennial, the journey to financial independence may seem daunting, but investing in your future is key to achieving your goals. Start by understanding the power of compound interest. By investing early, even small amounts can grow significantly over time. Consider setting up a retirement account or investing in stocks or mutual funds that align with your financial goals and risk tolerance.

Diversifying your investments is crucial to manage risk. Spread your money across different asset classes to protect against market fluctuations. It’s essential to regularly review and adjust your investment portfolio to ensure it remains in line with your objectives. Remember, investing is a long-term strategy, so stay committed and patient through market ups and downs.

Embrace the digital age by exploring investment apps and platforms that offer convenient ways to start investing with low fees. Take advantage of robo-advisors that can help you build a personalized investment plan based on your financial situation and goals. Educate yourself on investment strategies and market trends to make informed decisions.

Keep an eye on your spending habits and prioritize saving for the future. Cut unnecessary expenses and allocate that money towards your investment accounts. Building an emergency fund is essential to protect your investments during unexpected events and avoid the need to tap into your long-term savings.

Planning for Major Life Milestones

Financial independence is a key goal for many millennials, but achieving it requires careful planning for major life milestones. These milestones, such as buying a home, starting a family, or retirement, often come with significant financial implications that can impact your long-term financial stability.

1. Buying a Home

One of the major milestones in a millennial’s life is buying their first home. To achieve this, it’s important to start saving and investing early. Consider creating a budget, establishing an emergency fund, and researching the housing market to make informed decisions.

2. Starting a Family

Starting a family is another significant life event that requires financial preparation. From childcare costs to saving for education expenses, planning ahead can help alleviate financial stress. Look into insurance options and consider creating a will to protect your loved ones.

3. Retirement

While retirement may seem far away for millennials, saving for it early is crucial. Explore retirement account options like 401(k) or IRA, and aim to maximize your contributions to secure a comfortable retirement. It’s never too early to start planning for your golden years.

By preparing for these major life milestones, millennials can set themselves up for long-term financial success and achieve the financial independence they desire.

Conclusion

By practicing smart budgeting, investing early, and prioritizing financial literacy, millennials can pave the way towards achieving financial independence.

{kind=link}